What We’re Seeing in Mortgages & the Market Right Now

This week, we were joined at our sales meeting by Jason Friesen, Managing Partner and Mortgage Agent at Outline Financial, who shared his perspective and some timely data on where the mortgage market is heading.

Much like the economists we heard from last week, Jason does not expect an interest rate cut in 2026. The next Bank of Canada announcement is January 28, but for now, the message remains one of stability rather than relief.

What is shifting is the type of mortgages Canadians are choosing.

Back in March 2025, about 43% of mortgage holders were opting for variable rates, largely in anticipation of future rate cuts. Normal distribution of mortgages based on a 10 year average is that 24% of mortgage holders have a variable rate mortgage. Jason expects that as rates continue to stabilize through 2026, we’ll see even more borrowers move back toward fixed options.

One metric I always watch closely is mortgage arrears, and the numbers continue to tell a reassuring story.

While arrears have increased from just over 0.05% in November 2022 to 0.26% in November 2025, that’s still far from crisis territory. For context, mortgage arrears currently sit at 0.71% in the UK and 1.61% in the U.S. By comparison, Canada is holding up remarkably well.

Part of that resilience may come from our shorter mortgage terms. With 3–5 year renewals, many homeowners are regularly re-qualifying, especially if they change lenders, unlike in the U.S., where mortgage terms can run the full 25 or 30-year amortization.

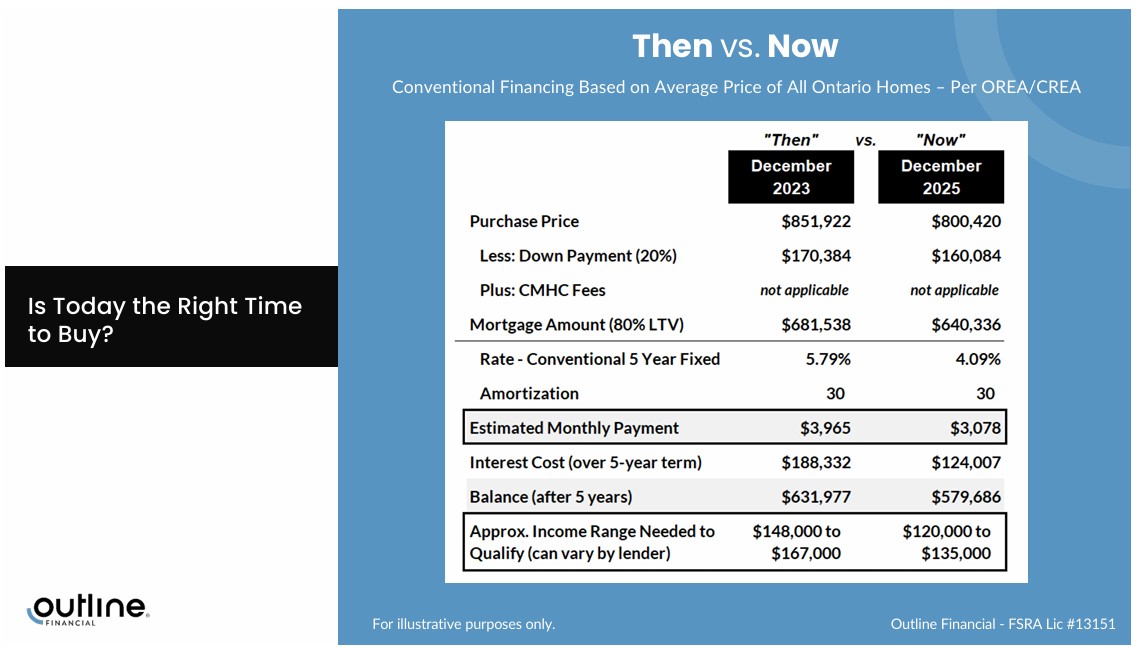

Outline Financial also shared a compelling comparison between buying in December 2023 versus December 2025. Today’s buyer, in many cases, is purchasing at a lower price and needs less income to qualify for the same mortgage amount than they did two years ago. Something that’s quietly improving affordability.

Looking ahead, roughly 40% of mortgages will be up for renewal this year, many of them originating at rates between 1.5% and 2.5%. Not every renewal will mean higher payments, it largely depends on how much equity homeowners have built up. The smartest move? Check in with your lender and speak with a mortgage broker for a second opinion to ensure you’re getting the best possible scenario.

What are we seeing on the ground?

On the ground, we’re starting to see some encouraging signs. This week, we re-listed a couple of condos and were pleasantly surprised by an uptick in showings. It’s early, but we’re hopeful this translates into more reasonable offers ahead.

Want to Make This Market Work for You?

As always, if you have questions about the market, or would like an updated home evaluation, we’re here to help.

For Sale: Renovated 1-Bedroom Suite in Yorkville, Toronto (40 Scollard Street #1502)

Across from the iconic Four Seasons, this fully renovated one-bedroom residence puts you at the centre of it all.Think morning spa treatments, chic brunches, and evenings spent exploring Toronto’s most coveted restaurants—all just steps from your door.

For Sale: 2-Storey Townhouse at King West, Toronto (12 Sudbury Street, #2212)

Welcome to a bright, generously sized two-bedroom condo tucked into the heart of Bloor West Village, just moments from the Junction.